Automotive Research Service

Already a subscriber? Log in here

Featured Research

Insights

Mobileye Revives Vertical Integration Strategy to Accelerate Robotaxi Business

Insight | 2Q 2026 | IN-8210

Fleet Intelligence Takes Center Stage at Ford’s 2026 Fleet Preview

Insight | 2Q 2026 | IN-8177

Auto China 2026 Establishes a New Competitive Baseline for EREVs

Insight | 2Q 2026 | IN-8169

Rethinking Cockpit Control in the Era of Touchscreens and AI

Insight | 2Q 2026 | IN-8124

As China Gears Up for Level 3 Autonomous Driving, the Rest of the World Remains Focused on Level 2++

Insight | 2Q 2026 | IN-8127

Latest Research

Report | 2Q 2026 | AN-6542

Presentation | 2Q 2026 | PT-3969

Presentation | 2Q 2026 | PT-3934

Market Data | 2Q 2026 | MD-EVB-105

Market Data | 2Q 2026 | MD-EV-105

Automotive Research Powers Technology Innovation & Implementation

Meet The Analysts You'll Work With

Dominique Bonte

Vice President

Matthias Foo

Principal Analyst

Leo Gergs

Research Director

James Hodgson

Research Director

Rachel Kong

Industry Analyst

Michael Larner

Senior Research Director

Adhish Luitel

Research Director

Ryan Martin

Senior Research Director

Dimitris Mavrakis

Senior Research Director

Michela Menting

Vice President

Jamie Moss

Research Director

Jake Saunders

Vice President

Phil Sealy

Research Director

Dan Shey

Vice President

Tancred Taylor

Research Director

Ryan Wiggin

Principal Analyst

Companies Covered

Our expansive automotive research covers leading companies, hot tech innovators, and emerging players in the industry.

Latest News & Resources:

Automotive

Whitepapers

Designing for the SDV

31 Mar 2026

NVIDIA GTC 2026: Extending AI Leadership

26 Mar 2026

32 Technology Companies Leading The Way In 2026

12 Feb 2026Charts & Data

.png)

Global Vehicle Sales

09 Mar 2026

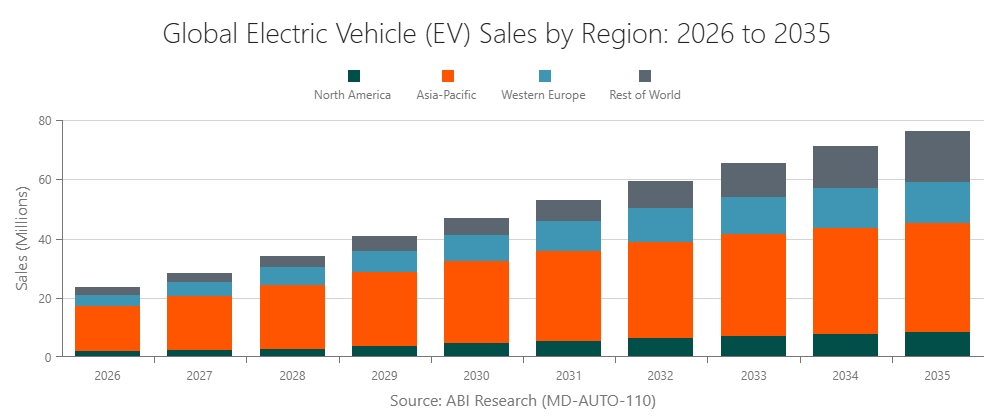

Global Electric Vehicle (EV) Sales

09 Mar 2026

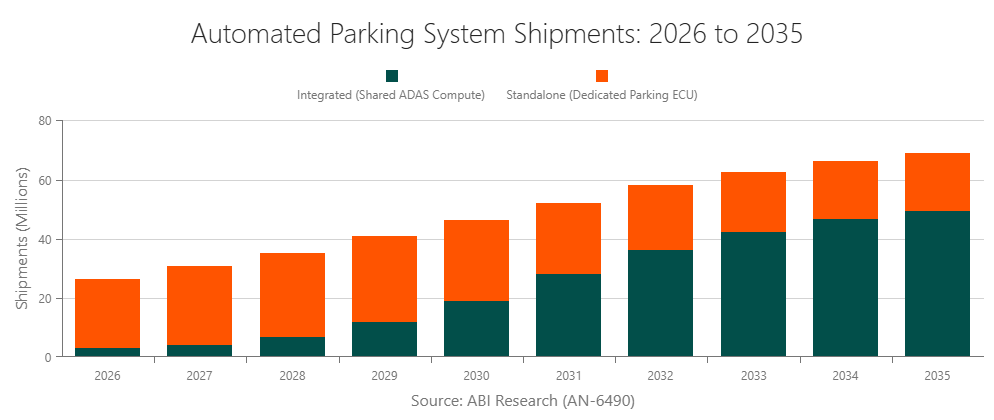

Automated Parking System Shipments: 2026 to 2035

26 Feb 2026

Blogs

Research Highlights

Deliverables

We cover the technologies, trends, and markets from every angle, and we deliver our qualitative and quantitative intelligence in multiple formats.

DATA

Market Data spreadsheets are composed of deep data, market share analysis, and highly segmented, service-specific forecasts to provide detailed insight where opportunities lie.

REPORTS

Our qualitative reports present in-depth analysis on key market trends, technologies, applications, and emerging companies. Reports are in PDF or PowerPoint format.

INSIGHTS

ABI Insights offer expert perspective on recent news events, including M&As, proposed and recently enacted regulations, product launches, and market updates.

RANKINGS

Competitive Ranking reports offer comprehensive insight into different markets, assessing companies’ implementation and innovation strategies.