A Subscriber Identity Module (SIM) is the nucleus of contemporary mobile devices as they authenticate user Identity (ID) for billing and store crucial identity information. As chronicled in ABI Research’s most recent SIM Cards market data report, demand for this technology has already passed its peak. Worldwide shipments for SIM cards (a combination of removable and Embedded SIM (eSIM) solutions) are set to plateau, growing at a Compound Annual Growth Rate (CAGR) of 1.5% between 2023 and 2028—reaching 4.67 billion units shipped by the end of the forecast window. For reference, 5.38 billion SIMs shipped in 2018.

The SIM card market has faced numerous challenges since 2019, and the latest macroeconomic woes have only added to the hardships for Consumer Electronics (CE) manufacturers and mobile operators. This resource will break down the most significant trends shaping the SIM card market in three periods: 2019 to 2020, 2021 to 2022, and 2023 and beyond.

Challenges Abound for the SIM Card Market, Even before COVID-19

It has already been established that the SIM card market went on a downward trend in 2019 and 2020. The market shrunk by -4.3% and -3.3% Year-over-Year (YoY) in those years, respectively. Even before the COVID-19 pandemic significantly disrupted the global devices market, three regional markets in Asia-Pacific (China, Indonesia, and India) were already adversely affecting the SIM card market. Consumers in China were given relaxed roaming fees in 2019, contributing to more widespread multi-SIM ownership per person. Around the same time, SIM card adoption in Indonesia dwindled due to Identity (ID) registration and a limitation of three SIMs per citizen. The story in India in 2019 was one where SIM supply lowered as the Mobile Network Operator (MNO) market consolidated and 4G promotions died down.

With the onset of the COVID-19 pandemic, conditions worsened for SIM card market players. Disruptions spread to production lines, supply chains, and labor shortages. These factors made logistics inefficient, which caused shipment delays, and weakened consumer device manufacturers’ next-generation product developments. The biggest ripple effects were felt within the 5G space, as production disruptions hindered the ability to develop affordable 5G handsets.

ABI Research reports that SIM shipments sat at 4.98 billion in 2020, with subscription contracts increasing from 18 to 24 months to 36 to 48 months.

SIM Card Shipments Continued to Dip in 2021 and 2022

By the time 2021 rolled around, the chip shortage was central to the SIM card market. While existing stock kept the effects of the chip shortage at bay in 1H 2021, the impact became more severe in 2H 2021, with SIM card IC deliveries being less than the 2020 figure.

Demand for SIM cards picked up in 2022, but the chip shortage impact had sustained. As a result, Average Selling Prices (ASPs) increased, disproportionately impacting various regions. More cost-sensitive areas like Africa and some parts of Asia-Pacific felt the greatest impact, while more developed regions were more resilient to the price increases.

The chip shortage and China lockdowns damaged SIM card supply chains badly enough in 2021, but emerging macroeconomic and geopolitical factors worsened things further in 2022. The SIM card situation was flooded with a seemingly never-ending stream of challenges, from rising energy costs to neon gas (used for manufacturing chipsets) shortages.

Between removable and eSIM, the SIM card market achieved 4.71 billion shipments in 2021, a YoY decline of -5.3%. And in 2022, ABI Research reports a further -5.6% decrease YoY, translating to 4.45 billion SIM shipments globally. It should be noted that the chip shortage predominantly affected the removable SIM card market.

Our Outlook for 2023 and Beyond

The year 2023 is another one filled with SIM card market challenges, although the dynamics and driving forces are somewhat different from those experienced in 2019 through 2022.

One primary market inhibitor is that of inflation, which continues to impact and set the backdrop economic tone of 2023. Ultimately, inflation is reducing consumer spending, which will have a direct knock-on effect on cellular device shipments as consumers look to cut spending and, thus, not renew handsets as regularly.

On a positive note, the ecosystem is beginning to emerge from the chipset shortage. Supply is beginning to return to normal levels as investments in increasing IC manufacturing capacity begin to be realized. On top of this is a softening in other high computing markets, such as CE devices, meaning additional chip manufacturing capacity is beginning to open up.

However, although demand softening in other markets might free up manufacturing capacity, the fact remains that many markets that are experiencing the softening are cellular in nature, so they require a SIM card. With devices like smartphones and SIM cards closely intertwined, any impact or softening in the smartphone market will likely result in a similar impact on the SIM card market.

For 2023, the SIM card market is facing a new chapter, when short-term demand falls, in line with cellular device shipments, but manufacturing capacity increases.

Generally speaking, the depiction of the SIM card market in 2023 looks pretty cloudy. Due to the emerging macroeconomic trends, ABI Research’s previous forecast of a +7.2% YoY growth has been adjusted to just -2.3%.

It's also worth closely watching how Apple’s Embedded Subscriber Identity Module (eSIM)-only smartphone devices perform in consumer markets. The first full year of Apple eSIM-only smartphone shipments into the U.S. market is 2023, and this is having an immediate and significant impact on the U.S. removable SIM cards market. For now, Apple’s eSIM offerings are constrained to the U.S. market, but the tech giant’s ambitions lie well beyond the American borders, with strong rumors building about Apple’s intentions to expand its eSIM-only smartphone range into other countries, most notably the United Kingdom, Germany, France, and Japan. In North America, ABI Research anticipates removable SIM card shipments to decrease by roughly 100 million in 2023 compared to 2022.

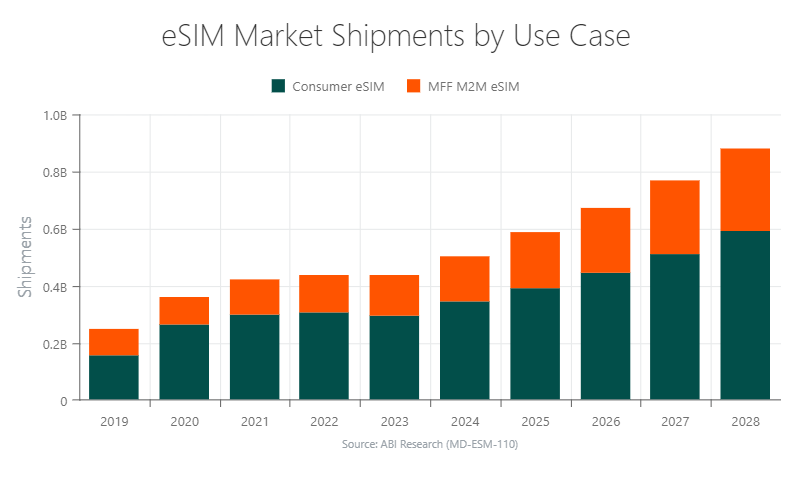

eSIM is undoubtedly “embedding” itself closer into the future of consumer electronics, so as the market propels forward, the demand for removable SIM cards will only be drained further worldwide. By 2028, 3.79 billion removable SIM cards will ship worldwide, well below the peak levels in the pre-2019 era. Meanwhile, eSIM shipments will grow at a CAGR of 14.9% between 2023 and 2028, totaling 881 million annual shipments by 2028.

Unlock the potential of the SIM card market with ABI Research's exclusive market data report. Our 5-year forecast will help your organization stay ahead of the competition by accessing comprehensive insights and analysis on the latest demand projections, segmented by region, country, form factor, vendor, features, type of memory, use case, and many more segments. Download the report today.

This SIM card market data comes from our Telco Cybersecurity Research Service, which you can learn more about by visiting the service page.

Sam Bowling

Sam Bowling