According to World Semiconductor Trade Statistics (WSTS), semiconductor manufacturing is expected to be a US$557 billion industry in 2023. In the wake of sweeping demand for semiconductors, manufacturers and their technology suppliers must accelerate their production processes, while balancing a tightrope between geopolitical trends and adhering to sustainability initiatives. The Asia-Pacific region remains a critical aspect of the semiconductor value chain; however, huge efforts in reshoring production plants (foundries) to North American and Western European soil are shaping a very different-looking industry.

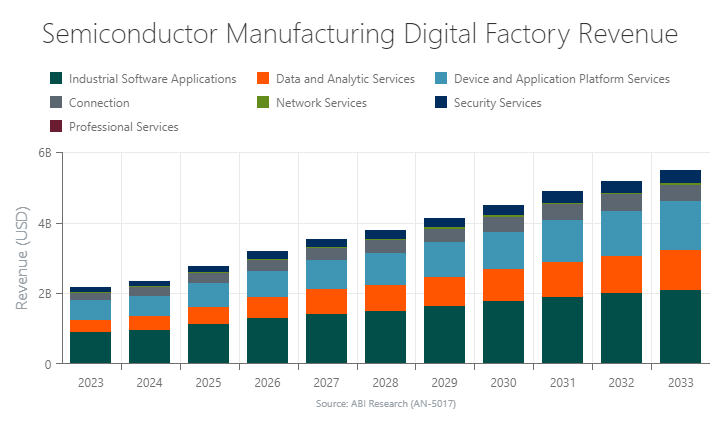

The chart below forecasts revenue generated from the various technologies that digitize semiconductor factories.

What Is a Semiconductor?

Semiconductors are a blend of thousands, even up to millions, of tiny transistors and electronic components arranged in a circuit on a silicon wafer. The function of the semiconductor is to execute a variety of tasks, such as managing electronics or processing, transmitting, and storing data.

There are four primary categories that semiconductors can fall under, including:

- Memory chips that store data and programs on devices.

- Microprocessors that act as the Central Processing Unit (CPU) for computer servers, Personal Computers (PCs), and smartphones.

- Integrated Circuits (ICs), which are used to perform repetitive tasks. Application-Specific Integrated Circuits (ASICs) can be created to suit a customer’s unique requirements.

- Single Systems-on-Chip (SoCs), which are chips that consist of all the electronic components needed for performing a task, such as integrating graphics into camera, audio, and video applications.

How the Semiconductor Manufacturing Process Works

The production of semiconductors involves eight major processes, as listed in the steps below:

Step 1: Wafer Manufacturing

Wafers are manufactured within controlled environments called cleanrooms, which are significantly cleaner than even a hospital operating theater. The primary material for wafer production is polycrystalline silicon, derived from sand. Initially, a cylindrical crystal ingot is formed, which is then meticulously ground to ensure a consistent diameter. Using a diamond saw blade, the ingot is sliced into thin wafers, completing the fabrication process.

Step 2: Process of Silicon Wafer Oxidation

The next step in the semiconductor production process involves cleaning the wafers using high-purity deionized water and carefully selected low-particulate chemicals. Subsequently, the silicon wafers undergo a heating process in an oxidation furnace, reaching temperatures of around 1,000° Celsius (C), while being exposed to ultra-pure oxygen. This controlled environment facilitates the formation of a uniform silicon dioxide insulator film on the surface of the wafer, ensuring consistent thickness throughout.

Step 3: Photolithography

To initiate the photolithography process, a light-sensitive film is applied to the wafer, imbuing it with properties akin to a photographic film. This crucial step of semiconductor production involves transferring the circuit's design onto the wafer's surface. A photo-negative equivalent is produced by developing the wafer, ensuring that the desired circuit pattern is accurately replicated.

Step 4: Etching

Excess materials are etched away from the wafer either via a wet etching process (with chemical solutions) or dry etching, which involves the use of gases or plasma.

Step 5: Deposition and Ion Implementation

In this step, a uniform thin film is applied to the wafer to give the chip electrical characteristics.

Step 6: Metal Wiring

This step enables electricity to flow through the wafer by depositing a thin metal film made of aluminum, titanium, or tungsten.

Step 7: Energy Dispersive Spectroscopy (EDS)

EDS is the process of testing the functionality of each chip.

Step 8: Packaging

The final step of the semiconductor manufacturing process is packaging. This includes cutting wafers into individual semiconductor chips that can be placed on a Printed Circuit Board (PCB) or in a device.

Largest Semiconductor Manufacturers

Based on market share, the largest semiconductor manufacturer worldwide is Intel, with a 12.9% market share as of 2021. The next four largest semiconductor manufacturers are Samsung (12.7% market share), SK hynix (6.2% market share), Qualcomm (5% market share), and Micron (4.9% market share).

Reference the table below to see the top-12 biggest producers of semiconductors.

Table 1: Semiconductor Manufacturing Market Share, 2021 (Sources: ABI Research; Infineon (2022/11/15 Infineon Investor Presentation, 2021 Market Size US$592 billion))

| Vendor |

2021 Market Share |

| Intel |

12.9% |

| Samsung |

12.7% |

| SK hynix |

6.2% |

| Qualcomm |

5% |

| Micron |

4.9% |

| Broadcom |

3.6% |

| NVIDIA |

3.5% |

| MediaTek |

2.9% |

| Texas Instruments |

2.9% |

| AMD |

2.7% |

| Infineon |

2.3% |

| Apple |

2.2% |

Semiconductors Serve as Vital National Security Interests

Everything from a new vehicle to a smartphone requires a semiconductor. In our digitally-fueled world, countries with a foothold in the global semiconductor market will gain a leg up over their geopolitical adversaries. Therefore, we are in the midst of a transformational phase in which Western nations, notably the United States, are taking the necessary steps to manufacture chips within their own borders.

The United States and China are trading blows to each other’s chip manufacturing capabilities. Regulations, tariffs, and sanctions run rampant within the semiconductor market, with the U.S. government considering bans on firms investing in and supporting China in technological innovation, including semiconductors.

For a better overview of the political themes interwoven into the semiconductor industry, consider the following government programs that encourage the design and production of semiconductors in their own countries:

- The Made in China 2025 program includes the greater production of semiconductors.

- The U.S. CHIPS Act reserves US$52 billion toward domestic semiconductor Research & Development (R&D) and manufacturing. An additional US$280 billion is planned for the next decade.

- The European Union (EU) Chips Act attempts to strengthen chipmaking capacity with funding reaching €30 billion.

- The Indian Government announced plans to spend US$30 billion to support local semiconductor production and enable a local supply chain.

New Semiconductor Facilities Being Built

Between 2021 and 2022, the investment in new semiconductor production plants exceeded US$300 billion, as per Semiconductor Engineering. Notable examples of these new facilities being developed include the following:

- Infineon: In November 2022, Infineon made a notable announcement regarding its investment of €5 billion in a new facility located in Dresden, Germany. The realization of this project is contingent upon securing sufficient public funding through the European Chips Act. If successful, the facility is projected to generate 1,000 job opportunities, with production expected to commence in 2026.

- Intel: Similarly, Intel revealed its plans in March, this time in Magdeburg, Germany, to invest €17 billion in a facility dedicated to producing transistor technologies. Production at this facility is anticipated to begin in 2027.

- Samsung: In November 2021, Samsung announced that it intends to invest US$17 billion in a facility situated in Texas. The facility is scheduled to commence operations in 2H 2024.

- Texas Instruments: Announced in November 2022, Texas Instruments plans to invest up to US$30 billion in constructing fabrication facilities for manufacturing 300-mm wafers. The operations at these facilities are set to begin in 2025.

- Micron Technologies: In October 2022, Micron Technologies disclosed plans to invest up to US$100 billion over a span of 20 years in a memory fab located in New York State. The facility is expected to start operations in the latter half of this decade.

- Semiconductor Manufacturing International Corp (SMIC): Moving to China, SMIC announced in August 2022 an investment of US$7.5 billion in Tianjin, aiming to establish production capabilities for 12-inch wafers with a monthly capacity of 100,000 units.

Something to be mindful of is that, as ambitious as these investments are, it takes roughly 2 to 3 years for new semiconductor plants to be fully operational after being built. Skills shortages are one of the biggest hurdles, with demand for workers in the semiconductor industry expected to increase by a million in the next decade, according to Deloitte.

Digital Transformation in Order to Keep Pace with Semiconductor Demand

Between 2021 and 2030, the market for semiconductors is expected to grow by 66%, making it a US$1 trillion industry, according to McKinsey. As semiconductors become more imperative to enabling digital experiences and embedding themselves into everyday life, fabless chip designers, manufacturers, and independent foundries must work closely with one another and digitally transform their equipment. Only then can the soaring demand for semiconductors be met by the chipset industry.

The development process of semiconductors, however, hinges upon numerous strategic considerations, such as having accurate demand planning, equipment predictive maintenance, operational visibility, etc. To gain the best course of action for both technology suppliers and semiconductor producers, download ABI Research’s Digital Transformation of Semiconductor Manufacturing research report. This content is part of the company’s Industrial & Manufacturing Markets Research Service.

Ryan Martin

Ryan Martin