The Vertically Integrated Era: What Rocket Lab’s Iridium Acquisition Means for NTN and D2D

By Andrew Cavalier |

06 Jul 2026 |

IN-8203

By Andrew Cavalier |

06 Jul 2026 |

IN-8203

Log In to unlock this content.

You have x unlocks remaining.

This content falls outside of your subscription, but you may view up to five pieces of premium content outside of your subscription each month

You have x unlocks remaining.

By Andrew Cavalier |

06 Jul 2026 |

IN-8203

NEWSThe Mega-Constellation Surge and Space Compute Shift |

On June 29, a definitive agreement was announced under which Rocket Lab will acquire Iridium for US$8 billion. While the acquisition is not expected to be complete until mid-2027, this deal will give rise to a new vertically integrated space company that has satellite manufacturing, launch, and operations all under the same business. Critically, Iridium is also the last of the Mobile Satellite Services (MSS) old guard holding globally coordinated L-band spectrum, critical for Direct-to-Device (D2D), Internet of Things (IoT), and Position, Navigation, and Timing (PNT), along with critical communications solutions. Alongside Iridium’s technical assets, the company boasts a 500+ strong partner ecosystem and 27 years of operating heritage to couple with Rocket Lab’s launch and manufacturing capabilities.

IMPACTThe New Space Model: Build, Launch, and Operate |

Rocket Lab is not a newcomer to space market, nor the value proposition of vertical integration. In fact, the company has been busy the past few years acquiring firms with key technologies to bolster the company’s technology portfolio.

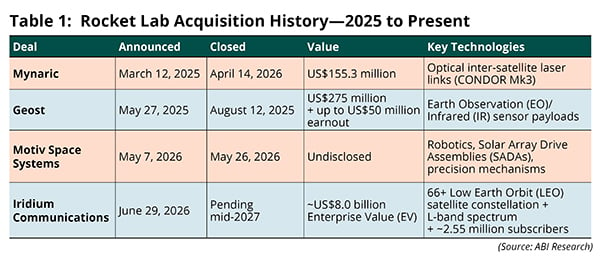

As Table 1 illustrates, Rocket Lab has spent 2025 to 2026 acquiring satellite payload and subsystem vendors, ranging from Optical Inter-Satellite Link (OISL) terminals (Mynaric) to EO/IR sensors (Geost) to robotics and precision mechanisms (Motiv Space). The pattern signals a long-standing intent to move beyond launch as the core business. In fact, the company already designs and builds satellite buses that customers can buy or that Rocket Lab operates on their behalf, with constellation work for clients including Globalstar, the Space Development Agency (SDA), and the Missile Defense Agency (MDA). The Iridium acquisition is a logical extension of its vertical integration strategy, giving Rocket Lab a working L-band LEO network, protected spectrum, around 2.5 million subscribers, as well as recurring revenue that would have been difficult to build from scratch. With Iridium’s foundational customers spanning aviation, maritime, government, logistics, energy, and remote industrial markets, the acquisition fast tracks the new company into a highly competitive position in the enterprise D2D and Non-Terrestrial Network (NTN) connectivity space.

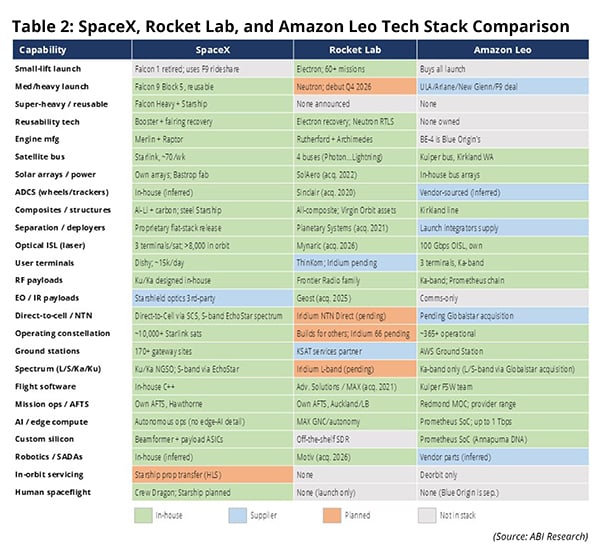

One of the clearest signals from this deal is that owning more of the space technology stack, launch, manufacturing, and operations has become the leading strategy for reaching commercial scale in the space market. SpaceX has been the template for this strategy, with launch capacity the industry's binding constraint; controlling it end-to-end has been a structural advantage, rather than just a cost saving mechanism. Table 2’s comparison maps three players disrupting the market against the stack. The depth of each company’s integration is a useful proxy for how well-positioned it is to compete as the market matures, even though full vertical integration also concentrates capital risk and execution burden on a single company.

Perhaps the biggest takeaway from these developments is that integrated space players are raising the bar across the space market. Pure space operators, especially those targeting LEO, may find themselves needing in-house manufacturing and launch, while pure launch providers may start hunting for applications businesses to attach recurring revenue. The merchant market opportunity is shrinking. The other reality is that SpaceX, and to a lesser extent Amazon Leo, have the balance sheets to make vertical integration look easier than it is. Rocket Lab is spending billions to absorb an aging narrowband LEO fleet, while simultaneously scaling Neutron and integrating four other acquisitions, a concentration risk that the strategy’s logic tends to obscure.

RECOMMENDATIONSA Shrinking Merchant Market and Rising Partnership Opportunity |

The increasing vertical integration by space leaders means the merchant market is shrinking for Original Equipment Manufacturers (OEMs), while partnership and acquisition opportunities are increasing for telcos. For space OEMs, the build in-house mentality among space companies will only escalate from here, and the question becomes which parts of the stack space operators won’t or can’t absorb. Those are the segments worth defending. This means that space OEMs should diversify their customer base toward players that aren’t integrating yet and move up the value chain from discrete components to integrated subsystems or modules that are harder for space primes to internalize. For telcos, licensed spectrum and their established subscriber base are strategic assets that space companies cannot easily build on their own, as the Iridium deal demonstrates. That leverage lets telcos negotiate to own a specific layer of the stack, rather than be disintermediated by it. D2D arrangements are the leading edge of this today, but this pattern is likely to extend into orbital compute, cloud, and AI training as new space systems enter service over the coming decade.

Written by Andrew Cavalier

Related Service

- Competitive & Market Intelligence

- Executive & C-Suite

- Marketing

- Product Strategy

- Startup Leader & Founder

- Users & Implementers

Job Role

- Telco & Communications

- Hyperscalers

- Industrial & Manufacturing

- Semiconductor

- Supply Chain

- Industry & Trade Organizations

Industry

Services

Spotlights

5G, Cloud & Networks

- 5G Devices, Smartphones & Wearables

- 5G, 6G & Open RAN

- Cloud

- Enterprise Connectivity

- Space Technologies & Innovation

- Telco AI

AI & Robotics

Automotive

Bluetooth, Wi-Fi & Short Range Wireless

Cyber & Digital Security

- Citizen Digital Identity

- Digital Payment Technologies

- eSIM & SIM Solutions

- Quantum Safe Technologies

- Trusted Device Solutions