NEWS

Decoding SpaceX's IPO Filing: Financials, Revenue, and Losses

|

On May 20, 2026, SpaceX publicly filed its S-1 registration statement with the U.S. Securities and Exchange Commission (SEC), and it is poised to be the largest Initial Public Offering (IPO) in history by capital raised (targeting up to ~US$75 billion), at a target valuation of US$1.75 to US$2 trillion. The largest IPOs, to date, by capital raised are Saudi Aramco (2019) at US$25.6 billion, followed by Alibaba (2014) at US$21.8 billion, and SoftBank (2018) at US$21.3 billion.

SpaceX’s stock (SPCX) is expected to have a target launch date in mid-June 2026 and a 5-for-1 stock split. This means that while investors will end up with 5X as many shares, the price of each share is reduced to one-fifth of the original value, hence the total value of the investment remains exactly the same.

Explosive Revenue Versus Cash Burn:

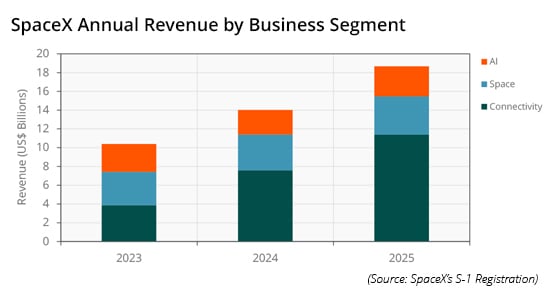

SpaceX’s business segments include the connectivity segment (Starlink), space segment (Falcon 9, Falcon Heavy, Starship), Artificial Intelligence segment (xAI and Grok).

- Total Revenue: US$18.7 billion for full year 2025

- Starlink Is the Cash Cow: US$11.4 billion in 2025, accounting for 61% of SpaceX’s total revenue. The launch services and AI segment contributed to US$4.1 billion (22%) and US$3.2 billion (17%), respectively.

- xAI Contributes to the Highest Operating Losses: The AI division is highly unprofitable and burned approximately US$6.4 billion in 2025, primarily driven by heavy Capital Expenditure (CAPEX) into AI infrastructure following its merger with xAI.

- The Anthropic Deal: Anthropic will pay SpaceX US$1.25 billion per month through May 2029, totaling nearly US$45 billion over the next 3 years. Anthropic aims to secure computing capacity for running its Claude AI software from SpaceX’s Colossus and Colossus II data center clusters.

IMPACT

What the IPO Means for the Future of Space, Connectivity, and AI

|

The Space Segment: Launch

- Mass-Production of Starship: In 2H 2026, Starship is expected to deploy Starlink’s next-generation V3 satellites that are designed to offer 1 Terabits per Second (Tbps) of downlink capacity per satellite. A single Starship launch will be capable of deploying up to 60 V3 satellites to Low Earth Orbit (LEO). According to SpaceX, one of its growth strategies depends on its ability to increase its launch cadence and payload capacity—both of which are highly dependent on the development of Starship.

- SpaceX conducted its most recent Starship flight (Flight 12) on May 22, 2026, which achieved its primary objectives, including deploying mock Starlink satellites, though the Super Heavy booster was lost.

The Connectivity Segment: Starlink Broadband, Starlink Mobile, and Starshield

The connectivity segment shows strong growth in 1Q 2026, generating a total of US$3,257 million. For the full year in 2025, the connectivity segment earned total revenue of US$11,387 million, with consumer accounting for US$7,208 million (63.3%) and enterprise & government accounting for US$4,179 million (36.7%).

- Starlink Consumer Broadband: As of May 2026, there are more than 10,400 Starlink broadband and mobile satellites in LEO and it will be deploying V3 satellites in the second half of the year using Starship, with a 20-fold increase in capacity added per launch versus the V2 Mini. This will greatly impact Starlink Broadband in terms of capacity and bandwidth capabilities, allowing it to compete more effectively with terrestrial networks, particularly in rural and remote areas. However, it remains constrained in terms of latency and network consistency, particularly when compared to terrestrial-based infrastructure.

- According to SpaceX’s filing, its broadband service offers a median latency at approximately 25 milliseconds (ms) and provides fiber-like download speeds at a median of 225 Megabits per Second (Mbps) during peak hours. It also provides download speeds exceeding 400 Mbps with round-trip latencies as low as 21 Milliseconds (ms).

- Bandwidth Comparison—Starlink Delivers Comparable Performance: In rural and remote regions, terrestrial alternatives such as Fixed Wireless Access (FWA) networks typically offer download speeds ranging between 50 Mbps and 300 Gigabits per Second (Gbps) depending on spectrum availability, network congestion, and cell-site density. While FWA deployments can achieve peak speeds, Starlink’s broadband performance—225 to 400 Mbps—positions it as a viable substitute in underserved regions, especially where the rollout of terrestrial infrastructure is costly and complex.

- Latency Comparison—FWA Outperform Satellite: FWA services typically achieve latency levels between 20 ms and 50 ms. In contrast, Starlink’s median latency of approximately 25 ms remains constrained by satellite orbital distance and signal routing paths, limiting its competitiveness in latency-sensitive applications.

- Starlink Mobile: According to SpaceX’s filing, Starlink Mobile has more than 30 Mobile Network Operator (MNO) partnerships covering an area that is home to approximately 1.9 billion people; Starlink Mobile will be a key contributor in the connectivity business. As of May 2026, there are more than 650 V1 satellites in orbit, providing data, voice, and messaging services to approximately 7.4 million monthly unique devices for Direct-to-Cellular (D2C) services.

- The funding boost from the IPO can fund the manufacturing and launch of the next-gen V3 satellites, allowing rapid scale of constellation capacity to expand Starlink Mobile and broadband services.

- Starshield (Government): Starshield is a secure satellite network designed specifically for government customers and national security applications. With public financial transparency through the IPO, this move will likely ease the minds of the National Aeronautics and Space Administration (NASA) and Department of Defense (DoD) regarding SpaceX’s long-term liquidity, resulting in higher investments and more complex mission profiles. With rising geopolitical tensions and instability, there is a higher demand for robust and persistent connectivity. Hence, Starshield will be a key component in driving SpaceX’s revenue in the connectivity segment, in addition to providing Earth Observation (EO), Intelligence, Surveillance, and Reconnaissance (ISR), and hosted payload capabilities for government and defense customers.

The AI Segment:

- Stabilizing the Cash-Burning Business Segment: A deal of up to US$45 billion with Anthropic right before the IPO validates and positions xAI as an infrastructure provider. It also signals a shift to Infrastructure-as-a-Service (IaaS) and a pivot toward becoming an enabler for other lead AI providers.

- Monetizing Underused Compute: xAI was, per internal-memo reporting, operating at an 11% Model FLOPs Utilization (MFU) rate, a measure of compute efficiency, well below the 35% to 45% typical of frontier training runs, meaning the bulk of theoretical compute throughput was being wasted due to heterogenous Graphics Processing Unit (GPU) architecture and the resulting straggler effect. Leasing the full Colossus 1 cluster (~220,00 GPUs, 300 Megawatts (MW)) to Anthropic helps monetize an asset poorly suited to xAIs’s own training requirements.

- Orbital Data Centers Potential Collaboration: As part of the Colossus 1 agreement, Anthropic also “expressed interest” in partnering with SpaceX to develop multiple gigawatts of orbital AI compute capacity (orbital data centers). This signals early customer demand for SpaceX’s nascent orbital data center segment, which today still largely exists as an FCC filing, but aligns with ABI Research’s outlook on the orbital data center market.

RECOMMENDATIONS

Winners and Losers Across the Connectivity Ecosystem

|

- Satellite Operators—AST SpaceMobile, Lynk Global, Globalstar, Amazon Leo, SES, Eutelsat OneWeb, and Others

- Consolidation Risk: The IPO will widen the funding gap for SpaceX, which allows the company to gain more access to capital markets. While the space industry is a high CAPEX market to break into. Smaller players with lower investments and funding will struggle to compete and risk being acquired by larger firms or forced out of the market. Over time, this will lead to consolidation in the market among a few dominant players.

- Increased Investments in the Wider Space Ecosystem: Investors may view the space industry with a new lens and drive greater investment into the broader space sector. A successful SpaceX listing could act as a sector bellwether, validating space as an investable category for generalist capital and lowering the perceived risk for startups with business models that depend on SpaceX's infrastructure (launch, Starlink, orbital compute). Over time, deeper private funding could strengthen the pipeline of credible vendors competing for government space contracts. However, a well-capitalized, public SpaceX may also raise the bar for smaller competitors in segments where it already leads.

- Telco Operators—T-Mobile, Verizon, AT&T, Rogers Communications, Orange, and Others

- Necessary Industry Partners: Telcos act as essential partners in the connectivity ecosystem. While SpaceX’s Starlink Mobile expansion plans have the potential to disrupt traditional carrier revenue models through its rapid constellation deployment and vertically integrated model that drives economies of scale, SpaceX has partnered with more than 30 MNOs as distribution partners. Today, satellite connectivity still struggles indoors for Direct-to-Device (D2D) services without a clear line of sight to the sky, making MNO partners a critical component of the D2D connectivity value chain. That said, Starlink Broadband is likely to emerge as the preferred connectivity solution in rural and remote areas, including the aviation, maritime and government sectors.

- Chipset Vendors—Qualcomm, Broadcom, MediaTek, Sony Semiconductor, and Others

- Huge Winners: As satellite connectivity at scale requires Non-Terrestrial Network (NTN) standards integration, it creates demand for high-performance satellite communication chips with embedded NTN standards protocols as part of their capabilities. In addition, these high-performing chipsets and modules will feature some form of edge Artificial Intelligence (AI) and compute abilities that support satellite connectivity at scale.

- Launch Providers—Blue Origin, Rocket Lab, Arianespace, and Others

- Launch Economics: With the IPO, investors will be able to compare launch margins and economics, reusability efficiency, and manufacturing throughput, among other key cost metrics. This transparency will expose the difference between SpaceX and its rivals—impacting the type of business (government, enterprise, research, etc.) that launch providers receive.

- Rival Comparison: For instance, Blue Origin’s New Glenn rocket experienced two major failures consecutively in 2026, destroying AST SpaceMobile’s BlueBird 7 in April during a second stage malfunction and damaging the launch pad in May during a pre-flight test. On the other hand, SpaceX’s Starship completed a successful test flight just a week before New Glenn’s explosion on the launch pad.

- AI Ecosystem

- Huge Winners: SpaceX’s ongoing data center operations rely heavily on energy, cooling, and distribution requirements, and the company plans to increase the scale of its terrestrial AI compute infrastructure. This is needed to support the increased AI workloads both in complexity and scale. The IPO will raise funding through public market liquidity to provide the compute capacity needed for scaling businesses. As a result, the greatest beneficiaries are likely to be AI developers, hyperscalers, enterprise adopters, and research labs (such as Anthropic) leasing data center capacity for their operations. These players will be able to gain access to additional computing capacity needed to train and deploy increasingly sophisticated AI models at scale.