NEWS

FCC Green Light, Launch Setback: AST SpaceMobile's Road to Commercial Operations Gets Complicated

|

Despite declaring its BlueBird 7 satellite a total loss, AST SpaceMobile hit a major milestone this month by receiving its Federal Communications Commission (FCC) approval to launch and operate its Low Earth Orbit (LEO) Direct-to-Cellular (D2C) satellite network. The approval grants AST the authority to deploy and operate its full requested 248-satellite constellation for providing Supplemental Coverage from Space (SCS) in the United States and D2C operations outside the United States. Critically, this means that it was simultaneously granted the SCS spectrum leases with AT&T, Verizon, and FirstNet in several bands:

All of this is AT&T, Verizon, and FirstNet’s existing terrestrial spectrum, leased or contracted to AST under the SCS framework—AST doesn’t hold this spectrum itself. Outside the United States, AST’s D2C operations use Mobile Satellite Services (MSS) allocations across the 617–960 MHz range under a separate International Telecommunication Union (ITU)-governed regime.

This all comes amid a rapidly shifting D2C landscape. The FCC has reinforced the incumbent MSS licensing structure, signaling that the existing spectrum moats are not up for renegotiation. Amazon announced a pending acquisition of Globalstar, which will hand it Globalstar's MSS spectrum licenses and position Amazon Leo as the new de-facto Apple satellite partner and a formidable future D2C entrant, with its own next-generation network targeting a 2028 deployment. Meanwhile, Starlink Mobile recently hit 10 million monthly users and has announced Gen 2 constellation plans using the New Radio (NR) Non-Terrestrial Network (NTN) standard targeting a 2027 deployment. Skylo has also reported millions of active consumer devices to date, while Lynk Global announced a merger with Omnispace and SES as a strategic backer—consolidating the D2C field.

While AST now has the regulatory clearance, the competition is scaling, the market consolidating, and the runway ahead looks far more contested than it did a year ago.

IMPACT

AST's Trajectory Is Disputed—Speed Is AST's Biggest Ally Now

|

AST has secured the regulatory foundation and significant carrier partnerships, but converting that structural advantage into subscribers before Starlink and Amazon Leo scale will define the company's trajectory in the North American market. While the company aims to launch another 45 to 60 satellites by the end of 2026, competitors SpaceX, Amazon Leo (pending the Globalstar acquisition), and Skylo all have operational services in the market today. Bringing a limited service to bear in 2026 with the current six BlueBird satellite constellation would still enable its partners to generate additional service revenue from its 248 million subscribers, albeit with limited geographic coverage and service windows. On the other hand, AST is competing with the T-Mobile-SpaceX alliance, which incentivizes competing telcos to prioritize their AST alliance, especially as the current business model allows AST spectrum access essentially in exchange for future service delivery commitments, with the Mobile Network Operators (MNOs) taking equity exposure via convertible notes.

The company’s anchor-partner model may save it a “seat at the table” thanks to its long-term partnership commitments with Verizon and AT&T, but the absence of exclusivity means that it will fight the competition for the same slice of the pie. Competitors are already providing their services today, so the U.S. anchor market strategy window is closing. Speed is AST’s best friend now. Perhaps AST already knows this, which may explain why it is making its most structural bets in Europe.

Incidentally, AST recently struck a deal with Vodafone to build a European Satellite Operations Center in Germany—a strategic bet on Europe’s appetite for sovereign space connectivity, which may create the moat it needs against global competitors. This is not a bad move, as Europe is a mature market with over 550 million mobile subscribers, high consumer purchasing power, and roughly 30% of the landmass has no cellular signal coverage. It’s an ideal home for a D2C operator willing to engineer sovereignty at the operational layer by handing European telcos the keys to the constellation, not just access to it. Timelines for regulatory approval and commercial service launch in the European Union (EU) could be expected by mid to late 2026, which is critical, as the competition has already built a foothold in these markets as well.

AST is running a dual-track strategy in which the U.S. relationships (AT&T and Verizon) are its core commercial anchor, and the European SatCo structure is a sovereignty-engineered variant designed to unlock a second major market. The "command switch" and German ITU filing aren't necessarily expressions of European independence from AST, they're the price of admission to European regulatory and political acceptance. The U.S. and EU stories are telling here, as these are core markets where AST maintains express commercial partnerships. In this respect, out of the 32 MNO partnerships that ABI Research has been able to verify for AST, 14 are Memorandums of Understandings (MOUs), which have much less commercial weight. When looking at the company’s position already being challenged in the core anchor market, this spread does bode well for the company’s long-term competitive positioning.

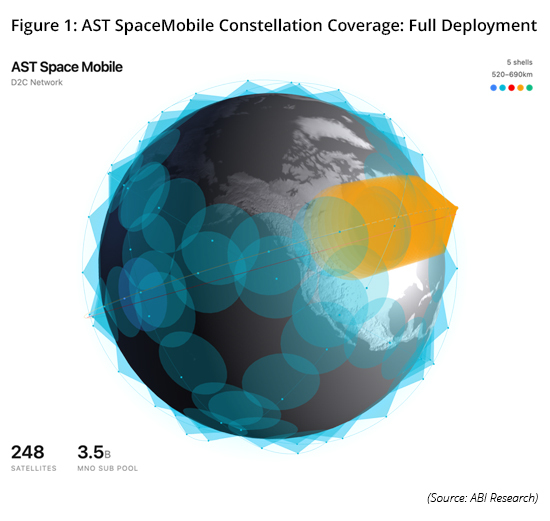

On the surface, AST still has a stake in the market. Its constellation, simulated with ABI Research’s internal constellation visualizer tool above, can provide overlapping coverage to a combined telco subscription pool of approximately 3.5 billion subscriptions across its announced MNO partners. Despite having fewer satellites than SpaceX, and with an assumed 20-degree elevation angle, the coverage area per satellite reaches between 3.63 million Square Kilometers (km²) and 5.59 million km²—a significant per-satellite coverage advantage over competing LEO D2C constellations. This coverage efficiency enables the company to accelerate a limited commercial service launch as early as 2026. Yet, despite the technical capability of any individual satellite, full commercial readiness can only be achieved through complete constellation deployment, with all 248 satellites operating in orbit. As the unsuccessful BlueBird 7 launch and an increasingly crowded competitor landscape illustrate, the window to capture market share and generate returns is closing fast—and what follows may be further market consolidation.

RECOMMENDATIONS

D2C Revenue Generation and Partnership

|

While AST stands at the precipice of a market that we expect will be worth over US$16 billion in service revenue by 2030, the opportunity pie is already shrinking. SpaceX’s increasing dominance and Amazon’s announced acquisition of Globalstar mean that two vertically-integrated juggernauts with deep pockets and device ecosystems have entered the fray. AST carries a track record of execution challenges, a rising risk profile, and growing carrier skepticism, so the competitive pressure is no longer technical or organizational. It is existential.

The AST story has yet to be written, but the signs of what’s to come are already being revealed in real time. Stakeholders in the D2C ecosystem can find a few key takeaways below:

- For Network Equipment Vendors (NEVs): At this stage, NEVs like Nokia and Ericsson should be doubling down on 5G NTN Radio Access Network (RAN) software stacks. While AST may be stuck with leased MNO spectrum in the United States, there is still an opportunity for the company to leverage the S-band outside of the United States in markets like the EU and Asia. Across the United States and EU, live 3rd Generation Partnership Project (3GPP) NTN-compliant services are already online with more expected to emerge by 2027. Both existing and prospective telco partners will need to be ready for this transition to deliver services to their subscribers. This is not only a future planning exercise; in many leading markets, integrating 3GPP NTN into telco networks is already underway.

- For Telcos: Telcos should develop a multi-vendor strategy for NTN. As seen with SpaceX in Ukraine and the uncertainty with AST SpaceMobile, the risk of overdependence on a single operator can create undesired exposure to the business and brand. Telcos are in a unique position with satellite NTN providers to negotiate favorable contract terms, as only a few MNOs structurally support NTN. But this will shift as satellite operators and their MNO partnership breadth scales across markets. Therefore, MNOs with national security exposure or sovereign customer bases should actively cultivate at least two satellite provider relationships across different orbit types, ensuring that no single provider can unilaterally affect service roadmaps.