NEWS

Amazon's Acquisition of Globalstar—Expansion of Network and Services

|

Earlier this month, it was announced that Amazon will acquire Globalstar for US$11.6 billion, which will enable Amazon Leo to add Direct-to-Device (D2D) services to its portfolio. The acquisition is expected to be completed in 2027, subject to regulatory approvals. Under this agreement, Amazon will acquire Globalstar’s existing satellite operations, ground infrastructure, assets, and Mobile Satellite Spectrum (MSS) licenses, including the L- and S-bands—a crucial advantage as they are authorized in over 120 countries. In addition, Amazon Leo has signed a new, separate agreement with Apple, offering satellite services for iPhones and Apple Watch, which were previously under an exclusive agreement with Globalstar.

Globalstar’s existing and new satellites will operate under Amazon Leo upon completion of the acquisition.

With the additional infrastructure and assets available to Amazon, the new capabilities will support the company’s long-term vision of space-based networks beyond terrestrial connectivity. Amazon Leo has a current constellation of more than 200+ satellites, with the full constellation planned at 3,236 satellites to be deployed by 2029. Amazon has also invested more than US$200 million in new facilities and infrastructure to increase its cadence of launches.

IMPACT

Formidable Competition with Leader SpaceX's Starlink—or Not

|

SpaceX’s Starlink D2C Rollout Strategy:

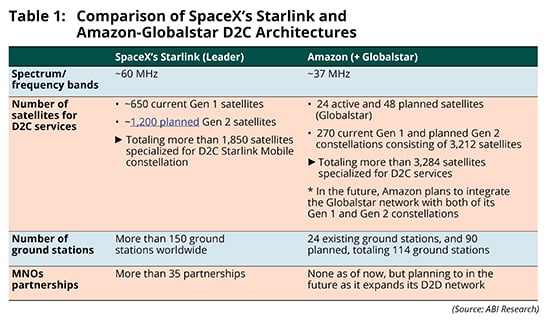

In 2025, Starlink launched more than 650 satellites for its Direct-to-Cellular (D2C) constellation and has connected more than 16 million unique users and more than 10 million subscribers as of March 2026. During MWC26 Barcelona, Starlink announced its Gen 2 Starlink Mobile constellation that will begin deployment in mid-2027. SpaceX plans to launch over 1,200 satellites within 6 months—with commercial services likely to see improvements in 2028. This upgraded constellation utilizes custom silicon and phased array antennas that are 5X larger than the previous version to deliver broadband-like speeds (up to 150 Megabytes per Second (Mbps)) and 20-fold improvement in link performance. As of early 2026, SpaceX operates more than 150 ground stations globally. Starlink also has a variety of spectrum bands for D2C:

- Hybrid spectrum acquired from EchoStar: AWS-4 Band/S-Band (40 MHz), AWS/PCS-H block/L-Band (10 MHz)

- Terrestrial spectrum from T-Mobile’s partnership: PCS-G block (10 MHz)

- Total of ~60 MHz spectrum for D2C services.

Globalstar’s D2C Planned Strategy:

Globalstar’s current network architecture consists of 24 satellites, with 17 planned launches in 2026. The satellite operator also has a new third-generation C-3 constellation (partially funded by Apple) planned at 48 satellites to expand capacity for commercial D2C services, consumer messaging, and Internet of Things (IoT), especially satellite features for Apple iPhones. Currently, Globalstar serves millions of iPhone users and had nearly 800,000 active subscribers by the end of 2025 for its MSS, which includes commercial IoT, asset tracking, consumer safety devices, and wholesale services.

What Will Amazon Get from Acquiring Globalstar:

By acquiring Globalstar, Amazon essentially has access to:

- Globalstar’s licensed MSS spectrum—L-Band (8.725 MHz), S-Band (16.5 MHz), C-Band (339 MHz; not for D2D)

- Globalstar’s terrestrial spectrum—Band 53/n53 (11.5 MHz)

- Total of ~36.7 MHz spectrum for D2C services.

- New software-defined satellites in the pipeline to be manufactured by MDA Space, which will then be integrated into the Amazon Leo network

- 24 existing and 90 new ground stations, totaling 114 ground stations.

This is on top of Amazon Leo’s existing Ku, Ka, and V-Bands, which are more suitable for high-speed broadband communications. The addition of n53, L, S, and C-Bands from Globalstar gives Amazon access to support D2C connectivity, directly competing with other satellite operators like Starlink, AST SpaceMobile, Lynk Global, Space42, and Skylo, among others.

Amazon’s Strategic Advantage Moving Forward:

With the additional frequency bands, infrastructure, and assets acquired from Globalstar, Amazon will have approximately 36.7 MHz of spectrum suitable for D2C services, as compared to Starlink’s 60 MHz of spectrum. This will evidently boost its D2C service capabilities planned for commercial service in 2028. However, service quality, capacity, and potential number of subscribers will depend on several factors, including the number of satellites, ground stations, and Mobile Network Operator (MNO) partnerships.

(Note: See more about the announcement of SpaceX’s ~1,200 planned Gen 2 satellites.)

As shown in Table 1, Starlink’s current D2C model relies heavily on MNO partnerships and leads in terms of its established infrastructure assets both in space and on the ground. However, Amazon will own globally-harmonized S-Band spectrum and an already operational network from Globalstar, which can bypass many regulatory frictions in international markets. In addition, its exclusive partnership with Apple gives it a competitive edge entering the market, as it will attain an immediate, high-volume consumer base. This move essentially helps to shave off time to market and accelerate the launch of its D2C services.

While Starlink has also acquired the S-Band from EchoStar and its customer base from Boost Mobile, it is expecting to test D2C services with the new spectrum by the end of 2026 pending final regulatory approval from the Federal Communications Commission (FCC), before launching a commercial live service.

RECOMMENDATIONS

Implications of M&A Activity on the Future of Commercial Space

|

Over the past couple of years, there have been a number of Mergers and Acquisitions (M&A) activities, with major players grabbing spectrum resources and market shares, and consolidating the space industry with a few formidable space players. Notably, examples include SpaceX/EchoStar, Lynk Global/Omnispace, Space42 and Viasat’s joint venture named Equatys, and the most recent Amazon/Globalstar.

The market landscape is seeing major shifts and consolidation as major players join forces to scale their operations and customer base. What might be some of the implications for the wider space sector?

- Boost in the Commercial Uptake of D2C Satellite Services: With emphasis and priority placed on D2C satellite services by service operators shown through spectrum grabbing, increased filings for satellite constellations, and M&A, fierce competition is expected through providing better service quality, expanding infrastructure assets, and accumulating more MNO partnerships. The stronger competition is likely to drive the Average Selling Prices (ASPs) down, which will boost the number of D2C subscribers and connections. Ultimately, customer retention will boil down to promising service reliability, Quality of Service (QoS), and proactive customer support when network issues arise.

- More M&A Activity to Take Place: Looking at the trend of M&A activity unfolding in recent years, major space players want to enhance their service capabilities for their customers and gain market share in the industry. It is likely that the space industry will consolidate and settle into a few dominant players—similar to the mobile industry in each country. Mergers will not only occur between satellite service providers, but they will also include the entire stack of the supply chain, from manufacturing to launch systems. It is possible that launch providers might be acquired by the bigger satellite operators for vertical integration to increase efficiency and lower costs of production.

- Rise of Sovereign Space Capabilities: Besides the commercial sector, governments recognize the significance of having their own infrastructure for critical connectivity, instead of relying on U.S.-based commercial giants. For instance, China possesses its own domestic satellite network infrastructure—BeiDou and Tiantong-1—and maintains an integrated system through partnerships with domestic MNOs such as China Mobile, China Telecom, and China Unicom to offer satellite services to the masses. Similarly, the European Union (EU) is developing its own sovereign satellite network (IRIS2) designed for secure communications. Self-reliance is what many nations hope to achieve, and we are likely to see a wave of “protectionist M&A” across other regions in the Middle East and Asia-Pacific, too.

- Increased Investments and Funding in the Space Sector: The space industry is no longer an “emerging” sector and has established itself as part of the core infrastructure surrounding other sectors, such as government, maritime, aviation, and consumers. For example, the EU’s IRIS2 project has a budget of US$12.6 billion designed to deliver competitive services alongside Starlink and Amazon’s LEO networks. In addition, Beijing Orbital Twilight Technology, a Beijing-based space startup, has secured early funding totaling US$8.4 billion from 12 major financial institutions as part of a wider push toward developing its space-based computing infrastructure. Many such investments and capital funding have been deployed to scale national and commercial space-based infrastructure.