By Malik Saadi | 02 Mar 2026 | IN-8078

Physical Artificial Intelligence (AI) was one of the most visible and referenced themes on Day One and Day Zero at Mobile World Congress (MWC) 2026. Multiple companies across the entire supply chain stack positioned Physical AI as the next step in the evolution of AI, linking it to transformative use cases and potential new revenue streams for Communications Service Providers (CSPs). The concept was presented as an enabler of intelligence moving beyond digital interfaces into real-world perception, coordination, and actuation.

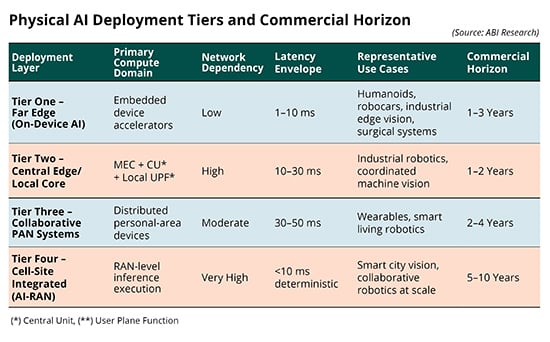

However, ABI Research discussions with various technology stakeholders at the show and prior to the show indicate that the industry is not aligned on how Physical AI should be defined. Interpretations vary significantly depending on the stakeholder. While narrative momentum is strong, deployment clarity and architectural consistency remain limited. Therefore, ABI Research structures Physical AI into four distinct deployment tiers to clarify timelines, latency requirements, and infrastructure dependencies.

Written by Malik Saadi

Chief Research Officer

Related Products

Edge AI Software Market Update: How Can Incumbent Hardware Vendors Drive Engagement?

Report | 3Q 2025 | AN-6486

TinyML: A Market Update

Report | 3Q 2022 | AN-5636

Electric Vehicle Charging Infrastructure Market Data Overview: 2Q 2026

Presentation | 2Q 2026 | PT-3935

Related Insights

Bringing Kubernetes to the Edge is Becoming Table-Stakes for Equipment Vendors

Insight | 2Q 2022 | IN-6524

AI Grid Pushes into Telco Networks and May Become the Most Important 6G Component

Insight | 2Q 2026 | IN-8108

Asia’s 5G Enterprise Opportunity Broadens: Singapore Accelerates 5G Edge Use Cases with MS Azure

Insight | 1Q 2023 | IN-6889