NEWS

Energy Shortage Motivates Orbital Data Centers

|

In late January 2026, SpaceX filed a plan with the Federal Communications Commission (FCC) to launch up to 1 million satellites, designed to act as Orbital Data Centers (ODCs) for Artificial Intelligence (AI) training. This will advance SpaceX’s launch plans, technology, and infrastructure several levels above its current Starlink constellation, which is a moderate fleet of approximately 10,000 satellites today. Although this plan is very ambitious and even labeled as “ridiculous” by other AI leaders, the energy shortage currently experienced by data center builders globally may well justify its existence.

Shortages driven by the AI supercycle are happening across the technology supply chain: these started with High-Bandwidth Memory (HBM)—the biggest infrastructure bottleneck—and then expanded to all types of memory due to collateral manufacturing constraints and Solid State Drives (SSDs), and even hard drives, with Western Digital and Seagate reporting being sold out for 2026 after selling their entire inventories to AI data centers. Nevertheless, the most pressing shortage is that of energy, which is split in two areas: generation and grid.

Energy generation is constrained by global demand, which is now compounded by new AI Data Center (DC) energy requirements. But the latter is not the biggest energy consumer globally. In fact, AI DCs are estimated to consume 5% of energy consumption in the United States today, which will likely increase to 10% in the next 5 years. The problem is getting energy to where it is needed. Grid demand has far outrun grid supply and, in some countries, the backlog to connect a DC to the grid can take up to 10 years. This is why new hyperscaler builds are relying on on-site energy generation via gas turbines (that are also facing shortages) and nuclear, as well as coal, both of which are markets currently being revived. Energy is now the biggest challenge facing the AI supercycle.

IMPACT

The Purpose of Orbital Data Centers

|

Elon Musk has stated that ODCs will not be used for inference or any other latency-sensitive workloads, but will excel in latency-tolerant training, which requires high degrees of computational processing and, of course, energy. Energy is abundant in space in the form of solar power, where the same Photovoltaic (PV) panel can create 5X to 8X more energy compared to a terrestrial installation. There is also the possibility of a Sun-Synchronous Orbit (SSO) that can keep satellites almost always illuminated, with uninterrupted energy. There are other considerations and challenges, including solar radiation, space debris, cooling, and many others, but there can be sufficient short-term technical progress to solve most of these in the SpaceX time frame. These technical challenges are somewhat similar to those faced by SpaceX with its Starlink constellation or Tesla with its Electric Vehicles (EVs), both of which have made major technical strides.

The SpaceX Chief Executive Officer (CEO) has also stated that in 30 to 36 months from now, the only scalable environment for new DCs will be space. This translates into an inflection point in 2029 or even sooner for ODCs to be justifiable. This is questionable at best, when new forms of energy generation will soon enter the fray, but the reason and true purpose of these ODCs is masqueraded.

RECOMMENDATIONS

TCO Comparison and Spillover Returns

|

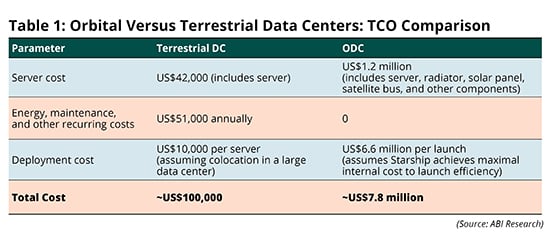

A brief Total Cost of Ownership (TCO) comparison from the ABI Research cloud and satellite teams indicates that the cost to launch a Graphics Processing Unit (GPU) in space is at least an order of magnitude higher than in a terrestrial DC. The team has modeled an H100 GPU to follow the Starcloud pilot launch and the simple modeling details are presented in Table 1.

Despite the simplicity of the TCO model above, the cost of delivery and space-hardening of the payload makes it financially impossible to justify, regardless of the energy shortage currently taking place on Earth. However, there may be other motives behind this push.

SpaceX has publicly updated its rideshare pricing—to lease rocket space to third parties—from US$6,000 to US$7,000 per Kilogram (kg) of payload delivered to orbit. ABI Research calculates that if SpaceX leases over 30% of its launch capacity to third parties and uses the remainder to deploy its own ODCs, it will have fully subsidized the entire launch and lifecycle costs of that network. In other words, the ODC pitch may well be an attempt to attract significant attention and capital investment to fund and accelerate an exponential increase in Starship production, which will, in turn, provide considerable network efforts for ODCs and many other adjacent areas.

The ODC pitch is arguably part of something bigger, as it cannot justify its existence only for AI training. On the other hand, the company is using multiple angles to justify its ambitious plan and even though it may not launch millions of ODCs, it will likely succeed in moving a share of AI training to space.